Inflation Targeting Essay

Inflation targeting is a monetary procedure in which the centralized depository approximates and makes open a probable, otherwise known as “target", inflation rate and then try to maneuver authentic inflation in the direction of the goal through the usage of interest rate alteration and further economic tools.

In 1990 it was originally accepted by New Zealand, the rules encircling the inflation targeting management have been so influential that almost every centralized depository have acknowledged that sustaining price constancy with inflation in the “diminutive solitary figure” is their lone mandate. Furthermore, price steadiness directs to continuous expansion and employment conception. Inflation targeting is frequently connected with modification in the centralized bank regulation that improves the sovereignty of the organization. In actual fact, while a small number of centralized depository accomplish the “model” of being “developed” inflation aiming organization, numerous other organizations focus on combating with inflation to the fundamental elimination of other objectives. Inflation targeting has developed into the central fiscal policy prescription for developing as well as industrialized countries equally. Inflation targeting in a variety of appearances has been taken up in latest eras by numerous developed states, such as the U.K, Finland, New Zealand, Canada, Sweden, Spain, Australia and Israel. (Bernanke and. Mishkin, 1997)

After the warfare, United Kingdom macroeconomic plan can be divided into dual years, related to binary principles, ancient and contemporary. By means of screening policy advancement taking into consideration these principles, it is feasible to clarify and bring together the announcement and proceedings of primary U.K. strategy creators, prior to and following 1979. The conventional alterations in the U.K. have not incorporated amendments in goals. (Nelson, 2008)

During the 1960s and 1970s, numerous researchers have disputed on the fact that United Kingdom’s strategy manufacturers deliberately selected elevated inflation assenting to an everlasting price increase/redundancy exchange. . (Nelson, 2008) The supporters of this disagreement have not supplied documents relating to the U.K. strategy manufacturers report. In actual fact, confidence in an exchange was not an element of U.K. strategy creators policy either prior to or following 1979. During the 1960s and 1970s strategy creators frequently and unambiguously discarded the thought of a swapping; moreover, their doctrine proceedings were not dependable with a Phillips curvature viewpoint. . (Nelson, 2008)It was an overhaul of set of guidelines and not distorted belief in a Phillips curve exchange that brought modification in U.K. economic guiding principle, and that overhaul of policy continues the foundation of inflation targeting in the United Kingdom. (Nelson, 2008)

Since the year 1992,The U.K’s fiscal plan can be portrayed as drifting swapping rates and inflation predicted targeting, through the intended assessment of inflation guiding to customer prices.( Nelson, 2008) A floating swapping rate provides the centralized bank the capability to utilize fiscal strategy to follow an inflation objective unswervingly, in a method that obligation to a permanent swapping rate does not, on the other hand, the exact responsibility and importance of the exchange/swapping rate in an inflation targeting command, for instance the United Kingdom’s, is a foundation of disputation, together in realistic strategy deliberations and inside the hypothetical text. According to Nelson “Understanding the reason for the changes in U.K. macroeconomic behavior is a matter of global interest.” (2008)).

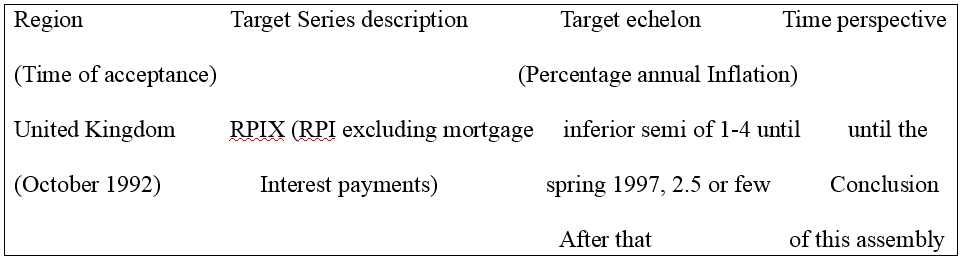

[Table I] Procedural characteristics of Inflation Targets: (Bernanke and Mishkin,1997)

The impulse for an inflation-targeting advancement has been diverse. In numerous situations, for example those of the U.K the fall down of a swap rate guided the economic regulators to look for a substitute. (Bernanke and. Mishkin, 1997) A number of standards, planned to relate to an extensive variety of situations, have been highly developed. Such as, an affiliate of the Monetary Policy Committee (MPC), which situates the temporary interest rate in the United Kingdom, has predominantly certified the standard that the exchange rate only concerns the fiscal strategy insofar as it has insinuation for the inflation predicament. Macroeconomic presentation in view of the fact that the beginning of inflation targeting in 1992 has almost certainly surpassed the prospects of the majority of analyst. In the U.K, RPIX inflation has normally been 2.6%, and Gross Domestic Product development has been 2.8%; from the time when depository self-government analogous statistics are 2.4% and 2.5 %.( Charles Bean, 2003).

One more characteristic of the United Kingdom model that should be emphasized is the responsibility that goes along with the judgment to assign procedural accountability for economic strategy to the MPC. There are three most important directions, primarily; the MPC is answerable to the Court of the depository, whose occupation it is to supervise the board’s progression although not its interest rate judgment. Subsequently, associates of the MPC emerge in front of the suitable group of congress, frequently soon after the Inflation Report has been publicized, to be inquired regarding the calculation following interest rate verdict. Prominently associates are detained independently responsible for their ballot. Thirdly, if inflation diverges in excess of 1 percent point from objective; the director is anticipated to inscribe an Open Letter to the Chancellor elucidating the reason as to why the divergence has taken place, what act is the board taking to convey inflation reversibly to the objective, and how that is constant with the government’s wide-ranging.

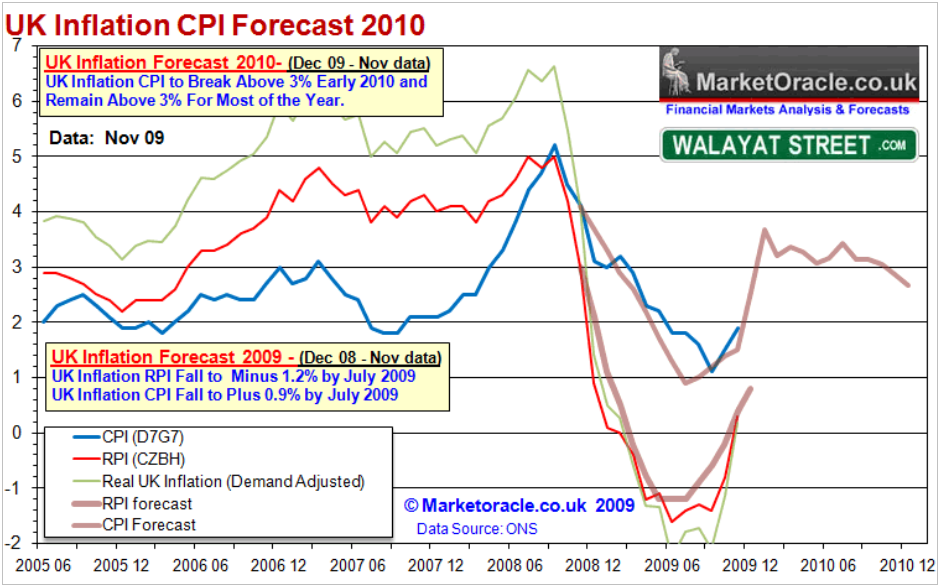

United Kingdom’s inflation forecast in 2010:

The current study for United Kingdom’s states that inflation elevated all through early 2010. This is in sequence with the examination that the Labor administration has thrived in a tough liability stimulated monetary revival that will turn out to be obviously noticeable all through the initial 3 months of 2010. UK inflation as calculated by CPI to split beyond the Bank of England's greater CPI objective of 3% near the beginning of the year, and continue on top of 3% for the majority of the year merely returning underneath 3% in late 2010 as an outcome of the subsequent administration endeavors to fetch the indefensible finances shortage controlled.

The figure below shows the current forecast of the inflation in U.K in 2010. (Walayat, 2009)

Table 2: (Walayat, 2009)

Advantages of Inflation targeting:

The most important benefit of executing an inflation- targeting rule that is also practiced in U.K is that it allows a state to achieve and sustain a small and steady rate of inflation directing to a number of advantageous outcome on monetary development. Furthermore, through the unequivocal mandate of the centralized depository to concentrate on attaining a small inflation rate, and moreover via the increased precision and answerability of economic guiding principle, the reservations amid remuneration and worth setters regarding the potential pathway of the inflation rate might turn down, and therefore, inflationary prospect might turn out to be more synchronized and precise. therefore, the centralized depository‘s attentiveness on an unambiguous inflation target might provide as a enhanced focus for earnings and value setting than in the case of economic or swapping rate targeting.

Secondly, the inflation target permits the centralized depository to develop its reliability by grants a sanitary orientation position regarding prices. It provides to substantiate the centralized depositary’s obligation to lower the inflation rate in the viewpoint of the community. Through announcing a quantitative objective or assortment, the centralized depository publicizes its obligation, which produces situations for much additional concentrated power of the inflationary outlook of marketplace partaker. Thirdly, the inflation targeting administration conveys an improved recurring alteration of the financial system for the reason that it leaves a considerable capacity for applying good judgment in practicing economic plan, and consequently allows the centralized depository to be extra supple in covenanting with amassed demand and supply alarm. A swap rate objective or economic targeting administration, on the contrary, might not be similar in temperament with counterpoise of the similar category of astound. . (Mishkin, 2007)

An additional benefit of an inflation-targeting administration is that once particular, it does not require to be attuned recurrently in view of the fact that it unswervingly centers on the concluding object. On the contrary, in case of the economic objective structure, the economic development objective might require to be attuned occasionally because there might be movement in the currency demand function effecting the association amid fiscal development and the value constancy objective.

Inflation targeting assists the centralized depositary in the U.K. to preserve lower inflation and that ultimately encourage long-standing development. A number of advantages of utilizing inflation targeting are as under:

- improved monetary expansion

- diminished relative cost inconsistency

- Low illogical redeployment along with

- Lower falsification inflation duty

Inflation targeting is an effectual fiscal strategy that offers improved ostensible anchor designed for fiscal strategy and inflation prospect. (Bernanke and. Mishkin, 1997)

Inflation targeting allows the centralized depository to position extended inflation aim. It escalates responsibility and financial strategy intelligibility. Paying particular attention to various irregularities. Time variation forces the authorities allowing long-standing effects of temporary proceedings.

As a result of these benefits, the inflation-targeting structure turn out to be, more convincing as compared with other governments It makes the operation of monetary policy more transparent, provides accountability, and contributes to the improvement and stabilization of investor sentiment. (Bernanke and. Mishkin, 1997)

Disadvantages of Inflation targeting:

In spite of the above mentioned benefits, the inflation-targeting administrations have some drawbacks. The chances that the central bank will be able to use its powers to correctly put in place the monetary policy are low. In terms of implementation, the inflation-targeting framework is much more complex than monetary targeting and exchange rate targeting frameworks.

The future looking character of an inflation targeting framework needs to consider the possibly extended intervals between modification in fiscal policy and its impact on inflation. Fiscal policy requires coping up with the divergence between the inflation targets and the inflation predictions at different strategy perspectives. The central bank needs to have an access to both an efficient inflation-prediction representation and strategy making mechanisms, which in turn influence the inflation predictions with rational accuracy. Additionally, given that the future looking character of an inflation-targeting framework carry a number of reservations into the policy conclusion, it allows additional powers to central bank than exchange rate or monetary targeting frameworks. Consequently, this kind of authority may permit policy makers to pursue excessively expansionary strategies. Even though the inflexible formation of the inflation-targeting administration offers an improved recurring modification of the financial system, this discretion may give way to incompetent productivity stabilization.

Contrary to the exchange rate or monetary targeting framework, it is not easy to manage inflation and the strategy mechanisms demonstrate their effects on price increases with extended and uneven intervals. With falling inflation rates, the main effects are on the developing countries. In such situations, big prediction mistakes and regular target overlooks are normally expected. Consequently, complexities are faced by the central bank in illuminating the causes of the divergences from the aim and in gaining trustworthiness, which is vital to the inflation-targeting administrations. Additionally, the preliminary disinflation procedures consequential from the starting of inflation targeting may increase immediate productivity outlay if personal representatives do not find the policy structure convincing right away. (Nelson, 2008) The inflation-targeting administration needs flexibility in terms of exchange rate, which normally leads to economic volatility. (Mishkin, 2007) The situation becomes predominantly severe especially when inflation rates are at very high levels and the administration is trying to bring them to low levels. In such situations, chances of mistakes with predicting the inflation are possibly great, inflation aims will have a tendency fail and the chances of gaining trustworthiness for the central bank from an inflation targeting policy are low. Keeping this in view, inflation targeting can be an efficient approach if it is implemented after there has been some successful disinflation. Another disadvantage of inflation targeting strategy can be the fact that it is not always adequate to make certain economic control or put a stop to economic power. It is still possible for administrations to follow reckless monetary policy with an inflation targeting rule in position. Huge monetary deficits will eventually be the reason of an inflation targeting administration to collapse: the economic deficits will ultimately have to be monetized or the public liabilities worn by a big deflation and inflation will increase. Nonexistence of absolute economic power is consequently a solution which is must for inflation targeting, and it is important to set up organizations that facilitate in keeping monetary strategy in check (Mishkin and Savastano, 2001). Likewise, a strong economic structure is one more requirement for achieving inflation targets as when economic mechanisms demolish, there is characteristically a rush in price rises in rising market countries. However, a strong economic mechanism and the nonexistence of financial supremacy are also vital to the maintenance and accomplishment of any economic plan, together with a exchange board or complete dollarization.

Conclusion:

United Kingdom’s fiscal strategy rule appears to have been in a position of continuous rebellion for a great deal of the time after the war. on the other hand, discover from the knowledge of other States, we now appear to have establish a position of institutional preparations and a fiscal strategy structure that have supplied to fetch a quantity of macroeconomic constancy to the United Kingdom that could by no means have been imagined the year in 1992. One of the two elements– the equipped self-government of the depository and an inflation target - the previous is possibly more essential. However the second has also been significant in serving lesser and steady inflation and in securing inflation prospects. Undoubtedly the globe will carry on flinging up novel tests to economic strategy manufacturer, in the U.K. and somewhere else. Our submission of inflation targets will require developing to convene those tests, but the present arrangement does, I consider, present a healthy and supple device in which to tackle them.